Why I Sold My Index Funds and Quit the Stock Market (Mostly)

In Antifragile, Taleb makes a barbell (bi-modal) argument for investing:

“If you put 90 percent of your funds in boring cash (assuming you are protected from inflation) or something called a “numeraire repository of value,” and 10 percent in very risky, maximally risky, securities, you cannot possibly lose more than 10 percent, while you are exposed to massive upside. Someone with 100 percent in so-called “medium” risk securities has a risk of total ruin from the miscomputation of risks. This barbell technique remedies the problem that risks of rare events are incomputable and fragile to estimation error; here the financial barbell has a maximum known loss.”

It mirrors something I’ve noticed with my more entrepreneurial friends who have dispensed with the common investment advice, advice I’ve given on this blog before and that you’ll hear from Tony Robbins and Ramit Sethi.

The advice goes like this. As you’re working, save your money, and optimize for more savable income. Since you won’t earn much interest in a savings account, it’s better to put it into a highly diversified portfolio of stocks and bonds using index funds from Vanguard or through a robo-advisor like Wealthfront. Assuming you’re properly diversified and we don’t get into World War 3, you should average out to a 5-7% annual return over a long enough time scale.

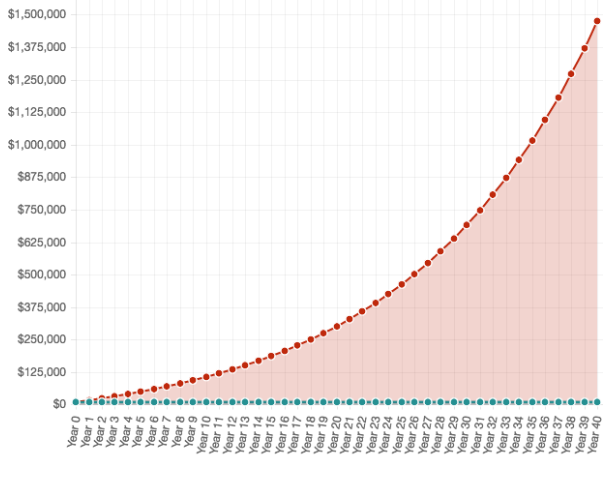

When someone gives this advice, they tend to show how with the magic of compound interest you can accumulate vast sums of money if you wait 30+ years [chart source]:

And it’s true. If you put in $10,000 today, and get an average 7% return with no taxes on it, in 30 years you’ll have about $76,000. If you don’t add any more to your initial principal, your money will roughly double every 10 years. In 10 years you’ll have $20,000, then 10 years to $40,000, then 10 years to $80,000.

The question you have to ask yourself, though, is could you double your money in 10 years on your own? And what other opportunities do you give up by making that money illiquid? For anyone with some interest in entrepreneurship, it’s hard to imagine you couldn’t successfully double your investment within 10 years.

Part of the challenge is the initial ramp up and money lost. On the Tropical MBA blog, Dan Andrews gives the “1000 day” rule for entrepreneurial projects replacing your salary. For the first 1,000 days, you don’t know what you’re doing and probably lose more money than you earn. After that, things start getting better, but you have to get through those first 1,000 days.

That is still only 3 years, though. And just because you lose money along the way doesn’t mean you can’t end up making even more in the long run.

Let’s take our $10,000 example again. Say that instead of investing it in the stock market, you were to invest it in teaching yourself new skills and trying to build a lifestyle business. To be safe, you give yourself a limit, spending no more than $1,000 to test each idea.

You could fail at the first 7 idea tests, then have the 8th one stick, and you would very quickly earn back your investment. The first $7,000 lost would have only been the investment in your learning. Better, you could do this all in the course of a year or two, earning back more than double your investment much quicker than you would get it in the typical index funds situation.

Along the way, you’re also in a less risky situation than the typical investment scenario. Since you’re keeping your money liquid, not in the market, you’re immune to sudden downturns. You don’t benefit from the bull markets either, but you don’t need to since you’re creating your own bull markets. It’s also a safer form of financial freedom since you don’t rely so much on consistent stock market returns. You’re relying on your own projects and investments you can influence.

It would seem that for someone sufficiently entrepreneurial, the typical investment advice isn’t a good use of your money, and you could err on the side of a more aggressive version of the entrepreneurial personal finance I’ve talked about before.

Even for someone not entrepreneurial yet, it’s not crazy to divest your personal investment account and put it into projects, so long as you’re being lean and not spending tens of thousands of dollars on an untested idea. You just might want to hedge it by continuing to contribute to your IRA, for example.

There are a few reasonable objections to this. The first is time. If you’re working a 40+ hour a week job, you might not have much time to dedicate to using your money this way. Then the question is, would it be better to keep the money liquid and wait for a good opportunity? Or put it in the markets until you feel you can use it?

I’m tempted to say keep it liquid and wait for opportunity to strike. I was discussing this idea with Justin Mares, and he pointed out how if he’d followed the conventional investment wisdom, he wouldn’t have been able to fund the first production run of Kettle & Fire on his own. The money had been sitting around going unused, but then he could invest a large chunk of it at once in what has now paid off many times his initial investment.

Another solution is to invest along the lines Taleb mentioned in the beginning of this article. You use a bimodal strategy of keeping 90% of your money in cash or equivalents, and then spend the remaining 10% on much more speculative investments like startup investing or cryptocurrencies. Then you’re still following the strategy, but betting on other people instead of your projects.

Another objection, or maybe we should say “reason people won’t do this,” is uncertainty misunderstood as risk. Putting money into a Wealthfront account is easy. Building a business or investing in a promising project is hard. It’s also much less clear of a path. For people who aren’t comfortable driving in the fog, the “throw money in Wealthfront and wait” route seems much less intimidating.

Building on the uncertainty is the locus of blame. When the market goes down and you lose half of your net worth, at least you can be pissed at Wall Street. When no one wants to buy your $300 imported poodle scarves and you have to shut down your Shopify store, you only have yourself to blame. Some people prefer owning the blame, but for those who don’t, this idea could be intimidating.

The last big issue is the amount of money you can mobilize this way. One benefit with the passive index investing is that it’s easy to do whether you have $10,000 or $1,000,000. You’d need to be constantly exposed to good opportunities and be able to keep investing in yourself and others to keep mobilizing your money this way, but that doesn’t mean it can’t be done, just that you have to keep watching for opportunities.

But all that said, if you have the time to work on projects using your money, if you can be smart about how you spend it investing in yourself and your work, and if you can handle being on the line for your own success, it might be worth considering liquidating whatever personal accounts you have (the non-tax advantaged ones) so you can invest in yourself. Or at least start with a portion of them and go from there depending on your success.

And yes, I sold all of my non-Roth-IRA index funds before writing this article. Sorry Wealthfront. Aside from keeping up the $5,500 annual contribution, I don’t plan to invest any more money in the markets.